Many people are worried about liability either through accidents or fraudulent lawsuits and are looking for a legal strategy to protect their assets. The best solution is highly relative to the situation of each individual. While there’s no one-size-fits-all solution, asset protection generally falls into three tiers. Each tier builds on the previous one, offering increasing levels of protection, complexity, and planning benefits.

If you need an asset protection structure and are interested in learning more, please give us a call!

What is “Protection”?

Before we dive in, it is important to clarify terminology. Often words such as “anonymity” get used when speaking about asset protection. Our firm prefers the term “privacy” over “anonymity.” Anonymity implies invisibility, which is not realistic. Government agencies and courts will always be able to identify you. Valid claims will result in discovery during litigation. We define privacy as the ability to keep your name off public records, limit easy access to your holdings, and raise procedural hurdles. These elements of privacy can deter baseless lawsuits, cut down on internet trolling, and make it less attractive for attorneys to take on a case against you on contingency. Simply put, privacy doesn’t make you invincible, but it significantly raises your level of protection.

Likewise, it’s important to understand that no asset protection strategy offers an ironclad guarantee. The goal is not to become untouchable, but to position yourself far more favorably in the event of a lawsuit. For example, a Wyoming domestic asset protection trust can, under most circumstances, prevent a judgment creditor from directly reaching the assets. However, long-term defiance of a valid judgment is rarely a sustainable outcome. What you can expect is that you will be in a significantly stronger position to negotiate a favorable settlement than if those same assets had been held in your own name. Asset protection doesn’t eliminate risk, but it shifts the balance of power.

Why Wyoming?

Wyoming is one of the strongest states for asset protection including:

- Domestic Asset Protection Trusts (DAPTs)

- Strong charging order protection for LLCs and trusts

- No state income, capital gains, or estate tax

- Strong privacy laws and low regulatory burden

- Clear statutes with trustee-friendly provisions

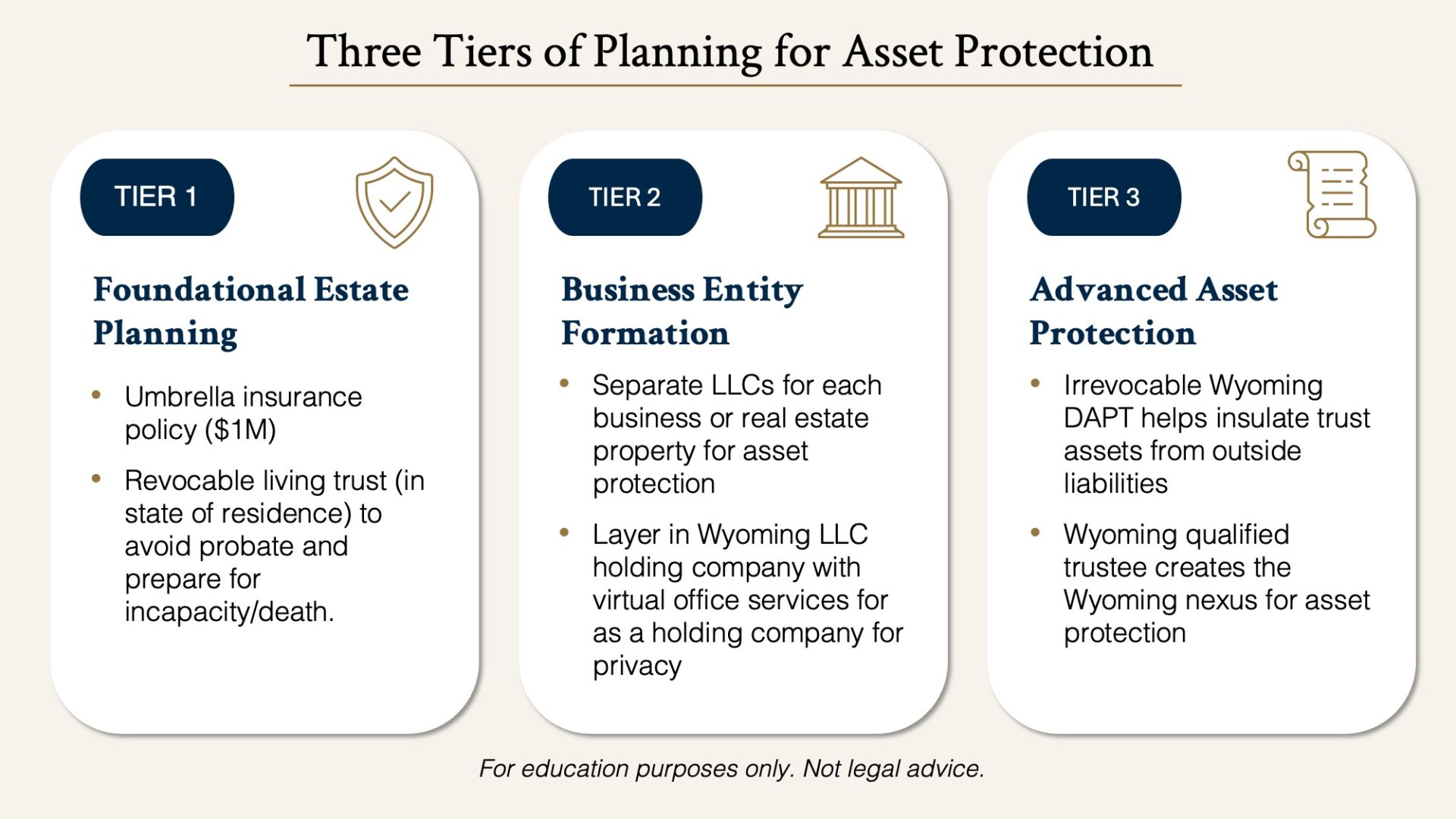

Tier 1: Basic Protection for Everyone

The first tier of asset protection consists of foundational tools that almost everyone should implement. These are affordable, simple to set up, and provide essential safeguards to your overall financial health.

Umbrella insurance is one of the easiest and most cost-effective ways to shield yourself from unexpected personal liability. This policy supplements your homeowners and auto insurance and can help protect your personal savings in the event of a major lawsuit.

A revocable living trust, while not a true asset protection tool, is a vital component of estate planning. It allows your assets to avoid probate, ensuring a smoother and more private transition of wealth to your heirs. It also makes it easier for someone to manage your affairs if you become incapacitated.

Together, these tools create a base level of preparedness that are helpful to nearly everyone.

Tier 2: Business Entity Protection

For business owners, rental property investors, and others with income-producing assets, forming a limited liability company (LLC) offers the next level of protection. This tier provides a legal firewall between your personal life and business activities.

A properly formed and maintained LLC limits your liability exposure, meaning your personal assets are typically not at risk if something goes wrong inside the business. In states with strong laws like Wyoming, LLCs also offer charging order protection, which limits what a creditor of a business owner can access. They may only receive distributions if and when they are made, and cannot force the sale of company assets.

LLCs also enhance privacy, especially when paired with a registered agent and virtual office. This keeps your name off the public record and makes it harder for potential litigants to find and target you.

It’s important to understand terms like Member (the owner), Manager (who controls the company), piercing the corporate veil (which courts may do if the LLC is improperly maintained), and tax election (an LLC can be taxed in several ways depending on your needs).

However, forming an LLC isn’t a one-and-done solution. You need to maintain separate accounting, keep up with annual filings, and document resolutions and meetings to preserve its protections. Enhancements like a two-tier structure (using a holding company) or having multiple members can further strengthen your position.

Tier 3: Advanced Protection with a Wyoming Trust

The third and most sophisticated level of protection involves setting up a Wyoming domestic asset protection trust (more technically called a Wyoming Qualified Spendthrift Trust or “QST”). This is an irrevocable trust governed by Wyoming law. Wyoming’s statutes allow a person to be both the grantor and a discretionary beneficiary of the trust. This provides a unique combination of protection and retained benefit. The settlor may retain the power to veto distributions, lifetime general and limited power of appointment, the ability to add or remove trustees, and the ability to act as investment advisor through a directed trust. These benefits add up to very powerful and flexible asset protection.

Are there Exceptions?

Wyoming asset protection trusts offer strong protection from future creditors by placing assets beyond the reach of most claims. However, there are some reasonable exceptions to this rule. First, fraudulent transfers (i.e. transfers made to defraud a known creditor) under the Uniform Fraudulent Transfer Act, are not protected. Consequently, any transfer of assets to such a trust must be accompanied by a qualified transfer affidavit, which includes a statement that the transfer does not render the settlor insolvent, that the transfer is not intended to defraud, and that the settlor maintains at least $1 million in insurance coverage. (W.S. § 4-10-510-523). Another exception is child support in arrears of at least 30 days. Lastly, financial institution have a claim to assets in a Wyoming asset protection trust if qualified trust property is listed on an application for credit.

Who Needs an Asset Protection Trust?

The Wyoming asset protection trust is best suited for high-net-worth individuals with high exposure to liability (such as physicians, developers, or executives), those with significant “spare” assets not needed for day-to-day consumption, and those approaching or exceeding the federal estate tax exemption. Assets placed in a Wyoming domestic asset protection trust may also be excluded from your taxable estate, depending on the structure.

Selecting a Wyoming Trustee

Many clients invest significant time and care in forming a Wyoming asset protection trust, but overlook equally important questions regarding its ongoing fiduciary administration.

Who Can Serve as a Trustee of a Wyoming Trust?

Wyoming statute requires that a qualified trustee reside in or be authorized to do business in the state in order to establish situs and benefit from Wyoming’s favorable trust laws. Under W.S. § 4-10-103, a “qualified trustee” must be a resident individual or a regulated entity authorized by the Wyoming Division of Banking to act as a trustee. The trustee must perform substantive trust administration within Wyoming, such as maintaining trust records, filing tax returns, or managing distributions (W.S. § 4-10-107-8). A Wyoming public trust company is often an ideal solution for those who want an efficient and professional trustee.

What Does a Trustee Cost?

Trustees typically charge a one-time set up fee as well as an annual fee based on several factors, including the nature and value of the trust assets, the complexity of those assets, the volume of transactions or administrative activity, and the scope of the trustee’s duties—whether the trustee serves in a fully discretionary capacity or operates as a directed trustee.

Why Wyoming Nexus is Important

Without sufficient connection to Wyoming, the trust risks being subject to the jurisdiction of another state. For example, the settlor’s state of residence may assert taxing authority or apply less protective asset protection laws. This exposure could undermine the effectiveness of the trust, particularly in the context of creditor claims or state income taxation.

What about a Wyoming Private Trust Company?

A Wyoming Private Family Trust Company, commonly referred to as a “PFTC” or “PTC” (W.S. § 13-5-601 et seq.) allows families to retain significant control over the administration of their trusts by serving on the board of the company that acts as trustee. This structure provides powerful benefits, including flexibility, continuity, and the opportunity to involve the rising generation in governance and stewardship.

However, a PFTC is not a mere formality. To preserve Wyoming situs and access the state’s favorable trust laws, the company should conduct substantive trust administration within the state, such as maintaining books and records, making distribution decisions, or holding board meetings. This will help ensure that the PFTC has a genuine operational presence in Wyoming, which entails governance responsibilities, professional support, and ongoing administrative costs.

What Assets Go into a Wyoming Asset Protection Trust?

The trust may be funded with a wide variety of assets, including investments, business interests, real estate, and intangibles. Many people wonder whether they can place everything they own into an irrevocable trust. The answer is that this is almost certainly not a good idea. You should not impoverish yourself to fund an asset protection trust because you will then need constant distributions from the trust. This sets up a very unfavorable fact pattern should you be subject to a lawsuit. We consider it a best practice to develop a contemporaneous financial plan that shows that the settlors were not dependent upon the assets transferred into the trust.

In summary, it is generally advisable to keep your primary residence, vehicles, and personal checking and savings accounts in your revocable living trust, where they remain easily accessible and under your direct control. Asset protection trusts generally work best when funded with excess assets, not essential ones.

Can You Place a Business in a DAPT?

Yes, but it depends. Whether or not you should transfer a business interest into a Wyoming asset protection trust depends on several factors:

- The value of the business – More valuable businesses make better candidates for protection.

- Where the risk is coming from – If the business generates the liability (e.g., customer lawsuits), the trust might not shield the value of the asset as expected.

- Your income needs – If you rely on the business for distributions, placing it in a trust may limit access or require careful planning to avoid tax or liquidity issues.

Final Thoughts

Effective asset protection isn’t about hiding behind an impenetrable wall, it’s about planning ahead, using legal structures wisely, and preserving flexibility while minimizing risk. The right strategy depends on your lifestyle, net worth, risk exposure, and long-term goals. Whether you’re just getting started with umbrella insurance or considering a Wyoming asset protection trust, each layer of protection builds on the next.

As always, we recommend working with a knowledgeable attorney to design a plan that’s tailored to your situation. If you’d like help evaluating your options or putting a structure in place, we’re here to help.

Frequently Asked Questions re Asset Protection

What is the asset protection law in Wyoming?

Wyoming law provides some of the strongest asset protection in the United States. It allows individuals to create a Domestic Asset Protection Trust (DAPT), more formally known as a Wyoming Qualified Spendthrift Trust (QST), under W.S. § 4-10-510–523. These statutes permit a person to be both the grantor and a discretionary beneficiary of the trust while shielding assets from most future creditors. Wyoming also offers strong charging order protection for LLCs, privacy safeguards, and no state income, estate, or capital gains tax.

Which state has the best asset protection trust?

Wyoming is consistently ranked among the top states for asset protection trusts, along with Delaware, Nevada, and South Dakota. Wyoming stands out because of its low fees, 1,000-year trust duration, strong privacy statutes, and flexible trustee-friendly laws. For many families, the combination of protection, privacy, and cost makes Wyoming a very competitive choice.

Can I make my assets completely untouchable?

No legal strategy can make your assets untouchable. The goal is to make them far more difficult for creditors or litigants to reach. A layered strategy helps avoid overemphasis on one particular strategy and allows you to scale your legal structure with your net worth and overall risk tolerance.

- Start with umbrella insurance and a revocable living trust.

- Add LLCs to separate business and personal risk.

- Use a Wyoming Asset Protection Trust (QST) for long-term security.

This approach won’t guarantee immunity, but it raises hurdles that deter lawsuits and strengthen your negotiating position.

What is the strongest asset protection?

There is no one-size-fits-all approach to asset protection, and there a few good jurisdictions. However, a strong form of protection is typically a Wyoming Asset Protection Trust combined with LLC structures. This setup allows you to retain certain benefits while placing assets beyond the easy reach of creditors. When properly structured and funded (without fraudulent transfers), it is one of the most durable asset protection strategies available in the U.S.

What is a major disadvantage of an asset protection trust?

The main disadvantage is loss of direct control. While Wyoming law lets you retain certain powers (such as acting as investment advisor or holding limited powers of appointment), the trust must have enough independence to be respected legally. Another disadvantage is cost: professional trustee fees, legal fees, and ongoing administration must be factored in.

What is the downside of putting assets in a trust?

The downside is that assets placed in an irrevocable asset protection trust are no longer freely available for day-to-day spending. If you rely heavily on those assets, frequent distributions can create an unfavorable fact pattern in court. That’s why we advise clients to place only “excess” assets into a DAPT, while keeping essentials, such as la primary residence, vehicles, and cash for living expenses, in a revocable trust.

What are common asset protection mistakes?

- Fraudulent transfers: moving assets into a trust when a creditor is already pursuing you.

- Improper LLC maintenance: mixing personal and business funds or neglecting records, which can lead to “piercing the corporate veil.”

- Overfunding a trust: transferring essential living assets you still depend on.

- Lack of Wyoming nexus: failing to keep substantive administration in Wyoming, risking loss of protection.

- DIY planning: using generic forms without legal guidance, which often leaves loopholes creditors can exploit.

How much does it cost to set up an asset protection trust?

Costs vary depending on complexity, but many Wyoming asset protection trusts involve:

- Legal setup fees: each attorney will have a different fee structure. Expect a cost that is much more significant than a revocable living trust or similar foundational estate plan document.

- Trustee fees: one-time setup fee plus annual administration fees, often charged as a percentage of assets or based on complexity.

- Ongoing compliance: costs for maintaining Wyoming nexus, such as registered agents, filings, or professional services.

What is the best form of asset protection?

The “best” strategy depends on your situation. For many enterprise families, possible actions include:

- Insurance as a first line of defense.

- LLCs for business and real estate holdings.

- A Wyoming Asset Protection Trust for long-term multigenerational security.

When layered together, these tools balance simplicity, control, and effectiveness.

Consult with a qualified estate planning attorney to assess your situation.

Who should consider a Wyoming Asset Protection Trust?

Doctors, executives, real estate investors, developers, entrepreneurs, and other professionals anyone with high liability exposure are prime candidates. It is also recommended for those approaching the federal estate tax exemption or with significant assets they want to preserve for future generations.

Can you put a business into a Wyoming Asset Protection Trust?

Yes, but it requires careful planning with an attorney. If the business itself is the source of liability (e.g., customer lawsuits), protection may be limited. However, for valuable, low-risk businesses, placing them in trust can provide excellent protection and estate planning benefits.

Disclaimer: The information provided in this post is for general informational purposes only and does not constitute legal advice.